How has it turned out for the universities?

The background

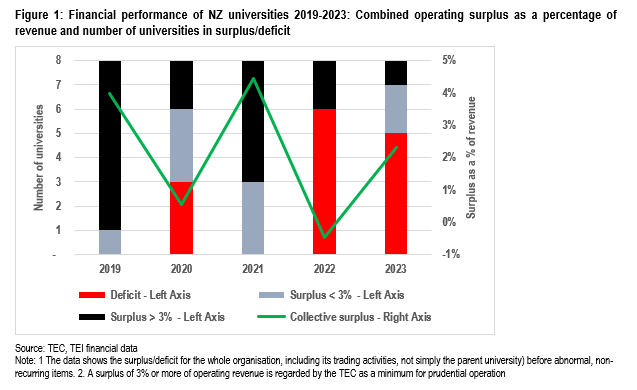

2023. Our eight universities were facing a bleak financial future.

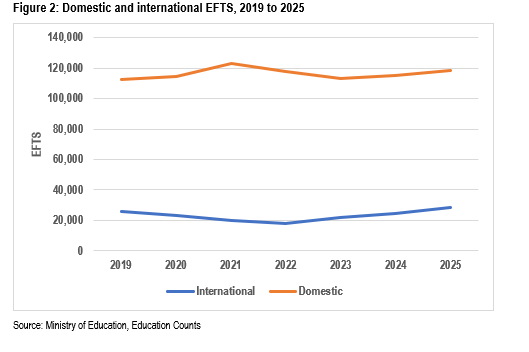

The pandemic meant international enrolments – an important contributor to university profitability – had fallen each year since 2019; by 2022, international enrolments were 30% down on pre-pandemic levels. In 2023, international students recovered slightly but were still only 84% of the pre-Covid level.

With the labour market weak in response to the pandemic, domestic enrolments had risen in 2021, but by 2022, that effect was evaporating; the labour market was very tight, fuelled by the government’s pandemic recovery spending. Domestic enrolments dropped 4% in 2022 and a further 4% in 2023.

Low international enrolments plus falling domestic ….

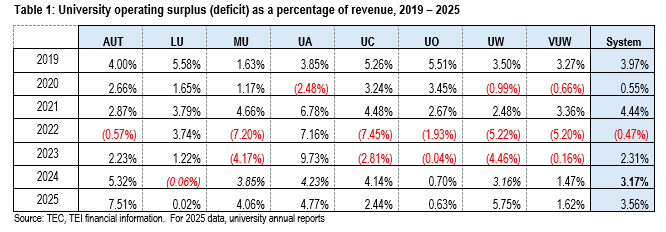

In 2022, six universities had reported deficits, and most were actively looking for savings across their operations. 2023 was nearly as bad – in the end five of the eight reported a deficit.

Take the University of Auckland out of the data in Figure 1 and the combined deficit was -4% of revenue in 2022 and -1% in 2023[1]. And when an institution is in deficit, it struggles to maintain – let alone enrich – its capability and its quality.

The University of Auckland apart, the financial strength of 2019 had evaporated.

While universities looked at innovative ways to maintain the breadth of their programmes and to maintain their capability, the minister (through gritted teeth) agreed to a short-term lift in funding for enrolments at degree-level and above …

I wrote about this here and here in mid-2023.

Could things get worse? Or was 2023 the nadir? The annual reports of the universities for 2025 are in. Three years on, how has it all played out?

Three years on

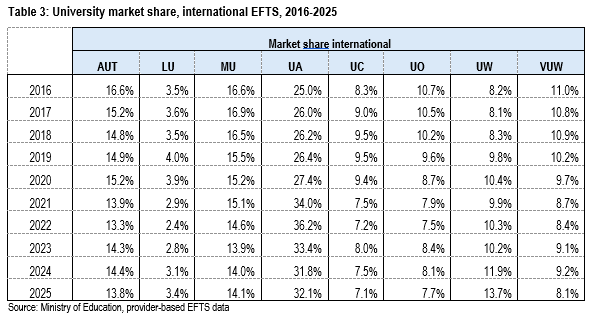

International enrolments are up …

Each international student generates around 60% more revenue than the average domestic student. That is why international enrolments are so important to university financial performance.

Across the system, international enrolments in 2025 were 11% above the pre-pandemic level, and up by 58% (around 10,000 EFTS) on the low point of 2022. Sure, the numbers were boosted by a new international foundation programme at the University of Auckland, phased in from 2020, that has grown to more than 1,000 EFTS; but even discounting for that, 2025 saw a 7% lift in international EFTS over 2019.

It’s not just the opening of borders that has strengthened the international market for our universities. New Zealand’s position may also have been helped by policy changes in our traditional competitors[2]. In the UK, Australia and Canada, concern about the scale of international education, housing constraints and a perceived risk of people using enrolments as a means of gaining permanent residency have led governments to tighten access for international students – including through limiting the number of visas, restricting students’ work rights and making it harder for students to bring their families and dependents with them. As for the US … Those factors are likely to have contributed to rising awareness of and preference for New Zealand as a study destination.

But the recovery in international EFTS has been uneven; international enrolments are up in the north, but down in the south; Auckland, AUT and Waikato have had comfortable increases on 2019 levels while Massey is fractionally above the pre-pandemic levels. But Victoria and the three South Island universities are still below their pre-pandemic levels[3]. Canterbury, Victoria and Otago (plus Massey) have lost market share while Auckland and Waikato have seen significant increases[4].

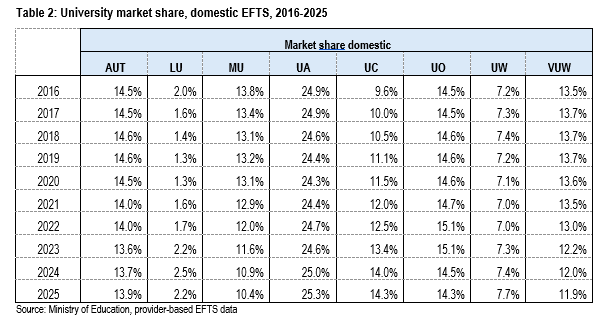

… while domestic EFTS have also risen …

Looking at domestic enrolments, the system was 5% up on pre-Covid levels but still 4% down on the peak pandemic enrolment in 2021.

The most notable trend among domestic enrolments since Covid has been the extent of the growth at postgraduate levels, mostly at the expense of bachelors enrolments.

Another interesting move has been the growth of the University of Canterbury among domestic enrolments – their share of the system’s domestic EFTS has risen every year since 2016, largely at the expense of Massey and Victoria – see the market share data in the table in the Appendix.

… leading to improved efficiency

A key driver of university financial performance is the student staff ratio – the EFTS to FTE ratio, with the EFTS figure weighted to reflect the higher revenue generated by international students[5]. The figure for the system has recovered from its 2022 low point, and, by 2024, was back to the 2019 level.

How does that translate to financial performance?

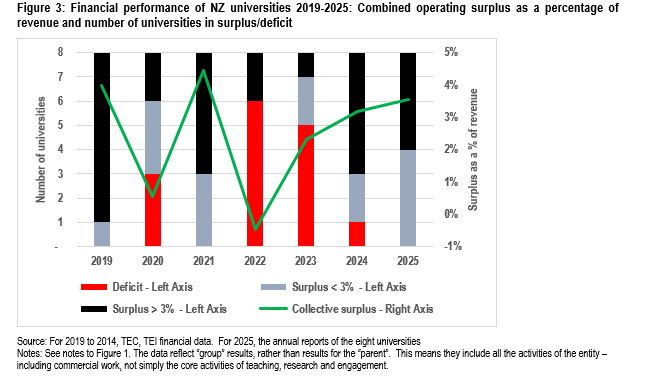

Let’s look at the annual reports for 2025. Here is what happens when we extend Figure 1 to cover the two most recent years.

It looks pretty good; all the universities are in surplus, four of them with healthy surpluses. And the collective surplus – 3.6% of revenue – looks reasonable. It’s not quite at the level of 2019, but close enough. The return of international students has made a difference. We can conclude that 2022/23 was the nadir …

But some universities struggle to generate a surplus on their core business …

But, looking closer, it’s not quite so simple. When we look at each university’s core business of teaching, research and engagement, three (Victoria, Canterbury and Otago) made a deficit that was offset by the earnings on their wider, commercial business (such things as their trading subsidiaries, returns on investments, facilities hire, catering, accommodation, contracting out expertise, ….). That repeated the pattern of 2024 – each of those three showed a deficit on core teaching and research paid for by surpluses on the associated business.

It’s no coincidence that those three have yet to regain their pre-pandemic international student enrolments and had a reduced share of the international EFTS. Canterbury keeps growing its share of the domestic market, but, with low international enrolments and falling market share, it struggles to generate a surplus on its core teaching, research and engagement.

Each international EFTS is worth 1.6 domestic EFTS … There are additional costs in recruitment and management of those international students, but there is still a substantial margin over domestic enrolments.

There is nothing wrong with using the surplus on trading to meet a deficit on teaching …

Relying on trading and commercial activities to generate a surplus is no bad thing. It makes sense; those activities exist for no other reason than to support the core work of the institution, financially as well as in other ways. And when the TEC does its analysis of the risks faced by institutions[6], it looks at the performance of the whole organisation, so it focuses on the group’s results, rather than the parent alone.

But it reinforces the importance of international students …

What the analysis suggests is the importance of the connection between international enrolments and the core business financial performance; it illustrates the contribution of international students to the financial health of a university, and hence, to building capability.

Our university model is critically reliant on international students.

The outlook

The enrolment outlook

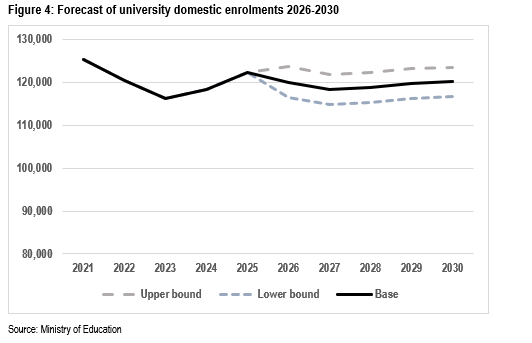

The Ministry of Education’s forecasts of domestic enrolments show university enrolments as dropping slightly then growing only marginally out to 2030.

There is little comfort for university managers in that.

The funding horizon

The Budget allows domestic fees to be increased by 6% (shifting the students share of the full cost of teaching from ~35% to ~36%). And the budget allows for most of the enrolments over institutions’ funding caps to become funded enrolments. But there is no tuition funding rate increase and no increase for the PBRF/TREF. By my estimate, those changes will lift total university system revenue by around $70 million a year, or about 1.4%, nowhere near the rate of cost increases.

At the same time, the science reforms (which aim to reduce the share of funding for investigator-led projects over time, and which will deliver greater focus on economic growth) will see universities’ income from government contestable science funds under pressure …. Those contestable funds may not contribute much to universities’ bottom lines[7], but they make a very valuable contribution to building capability and adding to research infrastructure in institutions.

Leaving …

… one source of revenue where the universities can exercise a measure of control – the recruitment of international students. Failing that, it’s a question of searching hard for savings and efficiencies.

The system has recovered from its 2022/23 crisis. But, over the next few years, all universities (but especially the four with lower surplus ratios – Victoria, Lincoln, Canterbury and Otago) face a difficult situation, one where the recruitment of international students becomes ever more important to institutional performance and thus, to system health.

Appendix: Data

Sources:

TEC: TEI financial data; Financial monitoring framework

Ministry of Education: Provider-based EFTS data; Enrolment forecasts

MBIE: Science Investment Plan 2026-2036

Education NZ: Brand awareness research

IDP: New visa rules for international students in 2026

University annual reports for 2025

Endnotes

[1] The University of Auckland’s surplus in 2021 was $90 million (7% of revenue), $98 million (7%) in 2022 and $151 million (10%) in 2022.

[2] See this THE article and this piece from international education brokers IDP.

[3] International EFTS at Victoria in 2025 were 11% below 2019. At Canterbury, the figure was 17%, at Lincoln 7% and Otago 11%. Victoria’s market share fell from 10.2% to 8.1%. Canterbury’s fell from 9.5% to 7.1%, Lincoln’s from 4% to 3.4% and Otago’s from 9.6% to 7.7%.

[4] See Appendix 1 for some of the data.

[5] See this paper which explores the correlation between student:staff ratios and financial performance

[7] Because history suggests that research project costs expand to fit the budget. Few make a substantial surplus.